Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The global system integration market attained a value of USD 507.17 Billion in 2025 and is projected to expand at a CAGR of 7.10% through 2035. The market is set to achieve USD 1007.04 Billion by 2035. The growing adoption of AI-enabled middleware solutions enhances real-time interoperability across heterogeneous IT environments, cutting manual integration time.

Most organizations are under pressure to unify their scattered IT ecosystems, spanning legacy databases, cloud-native apps, and edge systems, into a single, intelligent network. For example, IBM Corporation offers IBMi Modernization, an AI-enhanced platform that enables seamless orchestration between legacy enterprise systems and multi-cloud environments. The solution leverages quantum-safe encryption and automated workflow mapping to ensure data integrity while reducing integration latency.

In fact, according to the system integration market analysis, 88% of global enterprises are adopting hybrid integration strategies to connect on-premise and cloud resources efficiently. The emergence of real-time data pipelines, low-code integration tools, and event-driven architectures are collectively streamlining how systems communicate, enabling faster decision cycles and more agile IT environments.

Leading firms such as Accenture, Tata Consultancy Services (TCS), and Deloitte are developing modular integration frameworks that incorporate AI-driven observability and automated configuration. For example, in March 2023, Tata Consultancy Services announced the launch of its 5G-enabled solution, TCS Cognitive Plant Operations Adviser for the Microsoft Azure Private Mobile Edge Computing (PMEC) platform a self-adaptive integration layer that detects system inefficiencies and autonomously adjusts configurations across cloud-native and on-prem environments. Similarly, Accenture’s partnership with Google Cloud since April 2025, is enabling enterprises to modernize legacy ERP systems through AI-enabled middleware and microservice-based integration pipelines.

Base Year

Historical Period

Forecast Period

Compound Annual Growth Rate

7.1%

Value in USD Billion

2026-2035

*this image is indicative*

| Global System Integration Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 507.17 |

| Market Size 2035 | USD Billion | 1007.04 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 7.10% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 5.6% |

| CAGR 2026-2035 - Market by Country | India | 6.5% |

| CAGR 2026-2035 - Market by Country | China | 5.4% |

| CAGR 2026-2035 - Market by Service | Application Integration | 5.5% |

| CAGR 2026-2035 - Market by End Use | IT & Telecom | 5.7% |

| Market Share by Country 2025 | Japan | 4.3% |

The rise of distributed enterprises is pushing demand for hybrid and edge integration frameworks. With IoT devices generating petabytes of data daily, enterprises are deploying local integration nodes for real-time analytics. For instance, Microsoft’s Azure Arc and Google Distributed Cloud are expanding in industrial and telecom sectors to manage workloads securely at the edge. Apart from that, in May 2025, HPE launched a unified platform for hybrid cloud, cutting virtualization costs and boosting edge-to-cloud efficiency. Moreover, as per the system integration market research, 13% United States-based organizations have begun integrating edge and cloud data streams for synchronized analytics for greater ROI. This convergence is unlocking faster response times, better latency control, and new models of predictive maintenance across manufacturing and logistics operations.

Government-backed digital programs are becoming central to the system integration market dynamics. The United States Federal Cloud Computing Strategy (Cloud Smart) and India’s National e-Governance Plan actively promote inter-agency data integration to improve public service delivery. In Asia, Singapore’s Smart Nation initiative and Japan’s Society 5.0 push interconnectivity between AI, IoT, and data infrastructure layers, boosting growth in the market. These initiatives create long-term revenue stability for B2B integration service providers engaged in public digital projects.

Organizations increasingly rely on low-code or no-code integration tools to accelerate deployment cycles. Platforms like MuleSoft Composer and Boomi Flow allow non-technical teams to connect apps without deep coding expertise. For instance, since September 2025, Allot started leveraging SnapLogic to launch AI agent to highlight health inequalities in the pharmaceutical industry. According to the system integration market analysis, by 2026, 75% of large enterprises will use at least four low-code development tools for integration and process automation. This democratization of integration is reshaping the IT services landscape, enabling faster experimentation, reduced developer dependency, and greater scalability for mid-tier enterprises seeking digital agility.

As data integration grows, so do security concerns. Companies are embedding zero-trust architecture and integrated threat analytics directly into their system frameworks. For instance, Cisco SecureX and IBM Security Verify unify identity and network control across hybrid systems. In May 2025, the European Union Agency for Cybersecurity (ENISA) released a handbook with new interoperability standards for critical infrastructure operators, highlighting secure system integration as a strategic necessity, thereby propelling demand in the system integration market. Enterprises are investing in secure integration gateways to ensure compliance with frameworks like ISO/IEC 27001 and NIST-CSF, making security a core differentiator in integration projects.

Artificial intelligence is transforming how integration is executed and maintained. Tools leveraging AI-Ops and machine learning algorithms now automate anomaly detection, mapping, and data flow optimization. For example, IBM’s Watsonx Orchestrate, launched in May 2025, enables self-healing workflows by monitoring API latency and automatically rerouting data paths. According to the system integration market report, over 60% of enterprises will deploy AI-assisted integration tools to improve reliability and scalability. This trend reflects the growing push toward autonomous IT environments capable of managing complexity with minimal human intervention.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The EMR’s report titled “Global System integration Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Service

Key Insight: Infrastructure integration dominates the system integration market trends and dynamics with its stronghold in hybrid data and communication networks, while application integration accelerates enterprise modernization. Consulting services are evolving from advisory roles to strategic transformation partners, helping firms navigate digital complexity. Each service type strengthens organizational agility and operational intelligence. By blending legacy and modern frameworks, these services support interoperability, cloud migration, and cross-platform governance, providing enterprises with end-to-end visibility across functions.

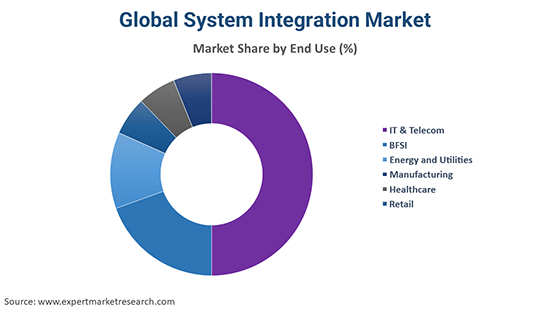

Market Breakup by End Use

Key Insight: Among all the end-use industries considered in the system integration market report, IT and telecom continue to anchor the market due to their deep technological reliance on integrated systems, while healthcare demonstrates unmatched growth from digital reforms and telemedicine adoption. Manufacturing firms are integrating automation with analytics to improve plant efficiency, while BFSI focuses on integrating fraud analytics and customer experience platforms. Energy and utilities invest in smart grid integrations, and retail sectors adopt cross-channel data integration for personalized customer journeys.

Market Breakup by Region

Key Insight: Regional adoption reflects different priorities. For example, North America leads with mature, enterprise-driven deployments, while Asia Pacific thrives on government-backed innovation and startup-friendly ecosystems. The system integration market in Europe maintains steady integration momentum through data privacy and cloud-interoperability standards, and Latin America focuses on industrial automation and fintech integration. Meanwhile, the Middle East and Africa are investing in smart cities and energy diversification projects that require end-to-end systems connectivity.

By service, infrastructure integration accounts for the largest share owing to hybrid cloud expansion

Infrastructure integration remains a cornerstone for enterprises modernizing legacy systems. Companies are rearchitecting data centers to integrate with SaaS, PaaS, and IoT environments as cloud migration is surging rapidly. System integrators are deploying cross-functional solutions combining DCIM (Data Center Infrastructure Management), Building Management Systems, and Integrated Communication networks to create unified infrastructure layers. For instance, by utilizing Generative Artificial Intelligence (GenAI), TCS extended its collaboration with SAP to facilitate business transformation in April 2025, boosting the overall system integration market value. Governments in North America and Europe are also funding “green data center” programs, which demand seamless integration of power, cooling, and automation systems.

The exponential growth of SaaS applications has spurred rapid adoption of application integration services. Reports suggest that enterprises now handle over 300 different applications on average, creating a critical need for unified workflows. Integration platforms as a service (iPaaS) such as Workato and Zapier for Enterprises are enabling organizations to connect disparate software ecosystems without disrupting daily operations. Moreover, with the rise of AI-driven data pipelines and unified APIs, application integration ensures seamless collaboration across CRM, ERP, and HR systems.

By end use, IT and Telecom lead the market owing to cloud modernization and network automation

IT and telecom firms are leading adopters of system integration, as they manage vast networks of connected assets and digital channels. With the rollout of 5G and edge computing, telecom operators are partnering with integrators to automate infrastructure management and improve service quality. For instance, Ericsson and Nokia have announced integrated OSS/BSS frameworks for telecom clients, enabling predictive network performance analysis. The sector also benefits from open-source orchestration platforms like ONAP, which simplify interoperability across vendors.

Healthcare is witnessing a strong growth in the system integration market, shifting toward integrated data systems that unify patient records, diagnostics, and remote care. The United States HITECH Act and the EU’s European Health Data Space have intensified efforts for interoperable digital health systems. For example, in October 2025, BD unified BD device data into a single intelligent ecosystem with the launch of the BD IncadaTM Connected Care Platform, a new scalable, AI-enabled cloud-based platform. Moreover, the growing use of AI-enabled imaging tools and telehealth systems demands integration across devices, cloud repositories, and healthcare applications.

North America holds the largest share owing to strong cloud and ai investments

North America leads the system integration market growth, propelled by investments in AI, cloud computing, and cybersecurity. The United States government’s Federal Data Strategy and Canada’s Digital Operations Strategic Plan are driving interoperability and data governance improvements throughout the region. Key players such as Accenture, IBM, and Cognizant dominate regional deployments, integrating AI-driven platforms with enterprise applications across sectors like defense, BFSI, and energy. The rapid expansion of smart manufacturing facilities and connected vehicle programs in the United States further fuels demand for seamless system orchestration, solidifying North America’s leadership in integration innovation.

The Asia Pacific system integration market revenue growth is accelerated by massive public investments in digital connectivity and automation. China’s 14th Five-Year Plan promotes cross-industry integration of AI and cloud infrastructure, while India’s Digital India and Japan’s Society 5.0 initiatives push interoperability in manufacturing, healthcare, and logistics. Additionally, Southeast Asian economies like Singapore and Indonesia are adopting national cloud frameworks to streamline citizen services and e-commerce systems.

| CAGR 2026-2035 - Market by | Country |

| India | 6.5% |

| China | 5.4% |

| Canada | 4.6% |

| UK | 4.5% |

| France | 3.8% |

| USA | XX% |

| Germany | XX% |

| Italy | XX% |

| Japan | 3.4% |

| Australia | XX% |

| Saudi Arabia | XX% |

| Brazil | XX% |

| Mexico | XX% |

Leading system integration market players are investing in verticalized offerings, cloud-native telecom stacks, FHIR-compliant health data fabrics, and OT-IT convergence platforms for industry 4.0, while niche specialists are capturing niche categories like API-security orchestration and edge data harmonization. Opportunities lie in productized integration blueprints, subscription-based integration maintenance, and ML-driven middleware that reduces manual mapping.

Further, strategic alliances with semiconductor, telecom and cloud providers are enabling faster go-to-market and joint IP creation. System integration companies that can package repeatable, compliance-ready solutions for regulated sectors, for example, pre-validated healthcare connectors or energy-grade grid orchestration modules, are finding steady revenue flow and higher margins, because customers prefer predictable deployment outcomes over bespoke, long-running projects.

Wipro Limited was established in 1945 and is headquartered in Bengaluru, India. Wipro is moving beyond classic systems work into outcome-based offerings that bundle cloud migration, AI Ops and industry accelerators. The company is developing modular integration kits for manufacturing and utilities that embed predictive maintenance and energy optimization logic.

Cognizant Technology Solutions Corporation was established in 1994 and is headquartered in New Jersey, United States. Cognizant is focusing on “techfin” and industry digital hubs, creating localized integration centers that combine fintech, cloud and security services. The firm is investing in composable integration platforms and industry-specific accelerators for banking and insurance, enabling rapid regulatory compliance and data orchestration.

Deloitte Touche Tohmatsu Limited was founded in the year 1845 and is headquartered in London, United Kingdom. Deloitte is leveraging deep consulting expertise to offer systems integration as part of strategic transformation programs. Its approach combines industry advisory, systems engineering, and managed integration services, with strong emphasis on secure data ecosystems and sovereign cloud adoption.

HCL Technologies Limited was founded in 1976 and is headquartered in Noida, India. The company is developing domain-specific integration factory models for telecom and manufacturing that include embedded telemetry ingestion, edge orchestration, and real-time analytics. HCL is emphasizing co-innovation with customers, offering platform-based services that let clients swap modules without full re-integration.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Other key players in the system integration market report include IBM Corporation, Capgemini SE, Cisco Systems, Inc., and Accenture PLC, and others.

Unlock the latest insights with our system integration market trends 2026 report. Discover regional growth patterns, consumer preferences, and key industry players. Stay ahead of competition with trusted data and expert analysis. Download your free sample report today and drive informed decisions in the market.

Upto 25% Off

USD

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

Get in touch with us for a customized solution tailored to your unique requirements and save upto 35%!

In 2025, the market reached an approximate value of USD 507.17 Billion.

The market is projected to grow at a CAGR of 7.10% between 2026 and 2035.

The market is estimated to grow in the forecast period of 2026-2035 to reach about USD 1007.04 Billion by 2035.

Stakeholders are prioritizing API-first architectures, investing in AI-enabled middleware, partnering with domain experts, standardizing data models, building modular deployment templates for rapid scaling and automated governance.

Growing technological advancements and increasing popularity of cloud-based technology are the key trends guiding the growth of the market.

The major regions in the market are North America, Latin America, the Middle East and Africa, Europe, and the Asia Pacific.

Infrastructure integration, application integration, and consulting are the leading services of system integration in the global system integration market. Infrastructure integration is subdivided by type into building management system, integrated communication, data centre infrastructure management (DCIM), and network integration, among others, while application integration is subcategorised by type into application lifecycle management (ALM), data integration, integrated security software, and integrated social software, among others.

The major end use segments of the product include IT and telecom, BFSI, energy and utilities, manufacturing, healthcare, and retail, among others.

The key players in the market include Wipro Limited, Cognizant Technology Solutions Corporation, Deloitte Touche Tohmatsu Limited, HCL Technologies Limited, IBM Corporation, Capgemini SE, Cisco Systems, Inc., and Accenture PLC, among others.

Integrators face legacy fragmentation, data privacy compliance, talent shortages in cloud-native skills, fragmented vendor ecosystems, and high customization costs that complicate scalable, repeatable integration deployments across enterprises globally and quickly.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Service |

|

| Breakup by End Use |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.

Share