Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The global silicon capacitors market attained a volume of 2415.60 Million Units in 2025. The market is expected to grow at a CAGR of 5.00% during the forecast period of 2026-2035 to reach a volume of 3934.76 Million Units by 2035. Growing emphasis on radiation-hardened components for satellites is largely propelling silicon capacitor innovations.

One of the primary driving factors reshaping the global market is the growing demand for miniaturised, high-reliability components in aerospace and medical devices. Silicon capacitors are becoming increasingly vital in systems requiring stable capacitance and low losses, especially under extreme temperature or radiation conditions. Companies like Airbus are expanding their procurement of silicon-based capacitors for space-grade PCBs as they offer unmatched durability in orbital environments. This particular silicon capacitors market trend is also backed by the European Space Agency’s (ESA) initiative to fund microelectronics research in space-qualified passive components, under its ARTES programme.

Moreover, the United Kingdom Government’s National Semiconductor Strategy announced in May 2023 is laying the foundation for advanced component development, including silicon-based innovations. The strategy aims to enhance semiconductor design and R&D capabilities in high-performance passive devices, directly benefiting firms involved in capacitor miniaturisation. Additionally, the United States CHIPS Act has also boosted silicon capacitor R&D with over USD 39 billion earmarked for domestic semiconductor production, encouraging innovation in sub-components such as ultra-thin capacitors, boosting the demand in the silicon capacitors market. As telecom and defence sectors shift towards 5G and LEO satellite communications, demand for silicon capacitors with high Q-factors and lower ESRs continues to surge.

Such structural investments coupled with rising electronic density per chip are creating a mature environment for silicon capacitor innovation, especially in high-frequency applications. With OEMs seeking robust performance at micro-scale, silicon capacitors are emerging as indispensable in multilayer module integration for next-gen electronics.

Base Year

Historical Period

Forecast Period

Compound Annual Growth Rate

5%

Value in Million Units

2026-2035

*this image is indicative*

| Global Silicon Capacitors Market Report Summary | Description | Value |

| Base Year | Million Units | 2025 |

| Historical Period | Million Units | 2019-2025 |

| Forecast Period | Million Units | 2026-2035 |

| Market Size 2025 | Million Units | 2415.60 |

| Market Size 2035 | Million Units | 3934.76 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 5.00% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 6.4% |

| CAGR 2026-2035 - Market by Country | Mexico | 5.8% |

| CAGR 2026-2035 - Market by Country | Saudi Arabia | 5.1% |

| CAGR 2026-2035 - Market by Distribution Channel | Online | 8.9% |

| CAGR 2026-2035 - Market by Application | Aerospace and Defence | 5.6% |

| Market Share by Country 2025 | Italy | 4.2% |

Silicon capacitors are witnessing increased demand in space electronics due to their resistance to radiation and extreme environments. Organisations like ESA and NASA are integrating these components in satellites, lunar landers, and deep space probes. For instance, the ESA’s JUICE mission utilises silicon capacitors in power conditioning modules. These capacitors outperform traditional MLCCs under thermal cycling and vacuum conditions. Moreover, global satellite launches, over 2,800 planned by 2030, are expected to stimulate further silicon capacitor consumption. Government-backed space programmes in India and Japan are now mandating component-level quality assurance, making radiation-tolerant capacitors a procurement priority in both public and private satellite ventures.

5G networks, particularly those operating in mmWave bands, require capacitors with extremely low parasitic effects. Silicon capacitors provide high Q-factors and ultra-low ESRs, essential for RF front-end modules. In addition, countries like South Korea and Germany are aggressively expanding their 5G infrastructure, boosting growth in the silicon capacitors market. In April 2025, Colt DCS expanded German footprint with EUR 2 billion data centre projects, where silicon capacitors will play a key role in filtering and impedance matching circuits.

As implantable medical devices like pacemakers and neurostimulators shrink in size, the need for ultra-compact passive components is expected to grow. Silicon capacitors provide a high capacitance density in a small footprint, making them ideal for such applications. In December 2024, Medtronic introduced a neurostimulator using monolithically integrated capacitors for enhanced power stability and longer battery life, accelerating the silicon capacitors market value. The United Kingdom’s National Institute for Health and Care Research (NIHR) also funded a study exploring the durability of silicon capacitors in biosensing implants. This R&D trend is encouraging component suppliers to develop biocompatible silicon-based passives tailored for medical standards like ISO 14708.

Electric vehicles (EVs) and ADAS systems require components with stable performance under wide temperature ranges. Silicon capacitors, owing to their stable dielectric characteristics, are increasingly being used in EV powertrains and sensor modules. EU’s Green Deal, coupled with the United Kingdom’s ban on new petrol vehicles by 2035, is pushing OEMs to integrate more robust passive components, widening the scope for silicon capacitors market expansion. This automotive push is fuelling not only volume growth but also the demand for customised silicon capacitor designs with integrated ESD protection.

With AI accelerators and edge computing systems demanding faster signal integrity, the role of silicon capacitors in high-frequency decoupling is expanding. Silicon capacitors offer reduced loop inductance and enhance transient response, which is critical in power delivery networks of high-performance processors. Intel’s latest AI chip platform uses embedded silicon capacitors to reduce power noise and improve performance. Furthermore, initiatives like the UKRI Digital Security by Design programme are fuelling demand for low-latency componentry in trusted computing.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The EMR’s report titled “Global Silicon Capacitors Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

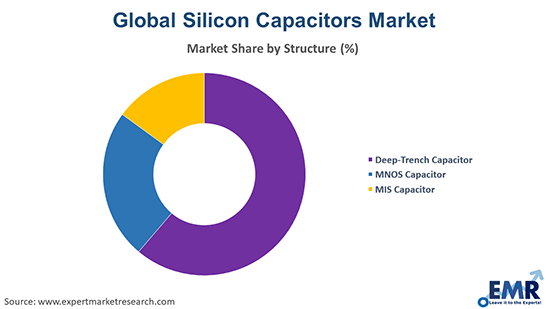

Market Breakup by Structure

Key Insight: Deep-trench, MIS, and MNOS capacitors all contribute to the silicon capacitors market growth, each serving a unique niche. Deep-trench types lead the global market due to their high capacitance density in micro packages, while MIS capacitors are finding rapid uptake in analogue precision circuits. MNOS capacitors, although niche, have become ideal for memory-related applications due to their charge retention capabilities. Their usage is also rising in radiation-prone environments, especially in space electronics.

Market Breakup by Distribution Channel

Key Insight: While offline distribution offers significant silicon capacitors market opportunities due to its role in high-reliability and mission-critical applications, online channels are disrupting the market through speed, accessibility, and platform integration. Both channels cater to distinct demand tiers; one focusing on customised and strategic supply chains, the other addressing rapid prototyping and standard inventory access.

Market Breakup by Application

Key Insight: Each application category is shaped by distinct performance demands. Automotive leads the silicon capacitors market due to EVs and safety system integration, while healthcare grows rapidly on account of implantable technology. Telecom leverages silicon capacitors for low-loss RF modules, aerospace demands radiation-hardened units for satellites, and other applications include precision industrial robotics and power converters.

Market Breakup by Region

Key Insight: While Asia Pacific dominates the global industry with production capabilities and demand from consumer industries, North America grows fast through government-backed innovation in defence and aerospace. Europe benefits from telecom and automotive innovation, Latin America from emerging medical and industrial applications, and the Middle East & Africa indicate gradual silicon capacitors demand growth in smart infrastructure projects. Each region’s growth aligns with its unique technological priorities and policy frameworks.

| CAGR 2026-2035 - Market by | Distribution Channel |

| Online | 8.9% |

| Offline | XX% |

| CAGR 2026-2035 - Market by | Application |

| Aerospace and Defence | 5.6% |

| Automotive | 5.3% |

| Telecommunication | XX% |

| Healthcare | XX% |

| Others | XX% |

| CAGR 2026-2035 - Market by | Region |

| Asia Pacific | 6.4% |

| Europe | 3.8% |

| North America | XX% |

| Latin America | XX% |

| Middle East and Africa | XX% |

By structure, deep-trench capacitor dominates the market owing to superior capacitance density

Deep-trench capacitors continue to dominate the global silicon capacitors industry due to their impressive capacitance-per-area ratio, which is critical for high-density packaging in microelectronic systems. These are particularly suited for RF and millimetre-wave applications where form factor and reliability are critical. Their low leakage current and compatibility with CMOS processes make them indispensable in telecom base stations and implantable medical devices. Additionally, Japan’s Ministry of Economy, Trade and Industry (METI) is funding domestic players to increase their vertical trench capacitor production.

Metal-Insulator-Semiconductor (MIS) capacitors are gaining traction for precision analogue applications due to their linear capacitance-voltage characteristics. Their rising adoption in DACs, filters, and high-accuracy timing circuits is accelerating the overall demand in the silicon capacitors market. Their lower process complexity and excellent integration with BiCMOS nodes make them popular among custom IC designers. United Kingdom-based universities in collaboration with NHS Digital are working on low-power diagnostic devices, pushing forward the development of low-drift, high-linearity MIS capacitors for medical-grade electronics and low-noise amplifier modules.

Offline distribution channels dominate the market due to custom supply agreements in aerospace & automotive

Offline distribution remains dominant, mainly due to long-term supply agreements between component manufacturers and OEMs in the aerospace, defence, and automotive sectors. Firms such as AVX, Murata, and Skyworks engage in offline partnerships to supply high-spec silicon capacitors with tailored parameters. These contracts often involve technical support, on-site testing, and non-standard form factors, which cannot be serviced via online portals.

As per the silicon capacitors market report, online platforms are quickly gaining popularity, especially for standardised silicon capacitors used in research, consumer electronics, and prototyping. Platforms like Digi-Key, RS Components, and Mouser have streamlined access to datasheets, certifications, and real-time inventory. These channels are also offering B2B-exclusive portals with custom filters, volume-based pricing, and just-in-time delivery systems, which appeal to R&D and low-volume innovators.

Automotive applications secure the largest share of the market due to growing EV and ADAS demand

The automotive application dominates the global silicon capacitors market, driven by the sharp rise in electric vehicles and advanced driver-assistance systems. These applications require capacitors with high-temperature tolerance, low ESR, and excellent reliability. Silicon capacitors have become a preferred choice for LIDAR systems, EV powertrains, and onboard charging modules. For instance, top-tier automakers are collaborating with capacitor suppliers to embed silicon passives in autonomous navigation systems.

The healthcare applications are significantly driving the silicon capacitors market revenue growth with the product’s growing application in implantable and wearable medical devices. Their miniaturised footprint, biocompatibility, and long operational life make them highly suitable for neurostimulators, pacemakers, and diagnostic patches. Innovations in bioelectronics and point-of-care devices have led to the adoption of ultra-thin silicon capacitors that enhance energy efficiency and signal clarity.

Asia Pacific commands the leading position in the market due to strong electronics manufacturing ecosystem

Asia Pacific is at the forefront of the global silicon capacitors industry dynamics, fuelled by its deep-rooted electronics and semiconductor manufacturing capabilities. Countries like Japan, South Korea, China, and Taiwan are home to several silicon foundries and capacitor manufacturing hubs. The regional focus on telecom infrastructure, EV development, and consumer electronics enables volume production and rapid innovation. Additionally, initiatives like Japan’s JASM project and China’s “Made in China 2025” strategy are injecting significant capital into advanced passive component design, which includes silicon capacitor technologies for high-frequency and power-sensitive circuits.

| CAGR 2026-2035 - Market by | Country |

| Mexico | 5.8% |

| Saudi Arabia | 5.1% |

| Japan | 4.5% |

| Australia | 4.3% |

| USA | 4.0% |

| Canada | XX% |

| UK | XX% |

| Germany | 3.6% |

| France | XX% |

| Italy | XX% |

| China | XX% |

| India | XX% |

| Brazil | XX% |

The silicon capacitors market in North America is witnessing strong growth owing to its rising investment in aerospace, defence, and semiconductor R&D. Silicon capacitors are increasingly used in space missions, advanced avionics, and critical communications infrastructure across the United States and Canada. Programmes like NASA’s Artemis and DARPA’s Next-Generation Microelectronics projects are directly supporting the development of radiation-hardened and ultra-reliable capacitor solutions.

Global silicon capacitors market players are focusing on custom engineering, integration in next-gen modules, and radiation-hardened technologies. Leading companies are investing in developing ultra-thin, high-density capacitor solutions for AI, automotive, and satellite systems. Strategic alliances with OEMs and government research agencies are becoming common, particularly for mission-critical applications. As market competition intensifies, opportunities lie in biocompatible materials, 3D integration, and embedded capacitor technologies for SiP and SoC packages.

Silicon capacitor companies are also leveraging AI-driven design tools for predictive reliability testing and optimising capacitor arrays for quantum computing hardware. The landscape is marked by agile R&D, patent race, and vertically integrated manufacturing to secure supply chain resilience. Companies differentiating through application-specific designs, including for neurostimulators or hypersonic navigation modules, are set to gain significant B2B traction. Moreover, regional expansion and compliance with aerospace and medical certifications are opening new verticals for specialist capacitor solutions globally.

Arrow Electronics, Inc., established in 1935 and based in Colorado, United States, plays a key role in distributing high-performance silicon capacitors through tailored B2B supply chains. It offers application-specific solutions to aerospace, automotive, and industrial automation OEMs by collaborating with niche capacitor manufacturers and integrating predictive inventory platforms for real-time order efficiency.

Murata Manufacturing Co., Ltd., founded in 1944 and based in Japan, is a key innovator in silicon capacitor technology. The company focuses on miniaturised and embedded capacitor solutions for telecom and healthcare electronics. Murata’s R&D centres actively collaborate with academic institutions to develop high-reliability passives for wearable and high-frequency systems.

Microsemi Corporation, established in 1959 and headquartered in California, United States, is known for designing radiation-hardened silicon capacitors. It caters to the aerospace and defence industry with components that meet stringent reliability and temperature resilience standards. Microsemi integrates its capacitors in satellite systems, radar modules, and missile guidance platforms.

Skyworks Solutions, Inc., founded in 2002 and located in United States, focuses on RF front-end innovation and uses silicon capacitors in 5G and satellite communication devices. Skyworks collaborates closely with telecom equipment manufacturers, offering compact capacitor arrays tailored for high-frequency performance and low signal loss in compact chip designs.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Other key players in the market are Vishay Intertechnology, Inc., and MACOM Technology Solutions Inc., among others.

Explore the latest trends shaping the silicon capacitors market 2026-2035 with our in-depth report. Gain strategic insights, future forecasts, and key market developments that can help you stay competitive. Download a free sample report or contact our team for customised consultation on silicon capacitors market trends 2026.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

Get in touch with us for a customized solution tailored to your unique requirements and save upto 35%!

In 2025, the silicon capacitors market reached an approximate volume of 2415.60 Million Units.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach almost 3934.76 Million Units by 2035.

Manufacturers are focusing on embedded capacitor R&D, forming OEM alliances, scaling aerospace-grade production, integrating AI-driven design platforms, and investing in regional compliance certifications to capture niche market applications and custom integration demand.

The key trends in the market are rising penetration of miniaturised electronic devices, and thin-film transmission lines with high RF (radio frequency) performance.

The major regions in the market are North America, Latin America, the Middle East and Africa, Europe, and the Asia Pacific.

Deep-trench capacitor, MNOS capacitor, and MIS capacitor are the various structures of silicon capacitors in the market.

The distribution channels include online and offline.

The various applications of silicon capacitors are automotive, telecommunication, healthcare, and aerospace and defence, among others.

The key players in the market include Arrow Electronics, Inc., Murata Manufacturing Co., Ltd., Microsemi Corporation, Skyworks Solutions, Inc., Vishay Intertechnology, Inc., and MACOM Technology Solutions Inc., among others.

The market is projected to grow at a CAGR of 5.00% between 2026 and 2035.

High production costs, integration complexities, and stringent aerospace or medical compliance requirements are hindering mass adoption of silicon capacitors, particularly in emerging economies with limited fabrication infrastructure and testing capabilities.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Structure |

|

| Breakup by Distribution Channel |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.

Share