Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The global pasta market was valued at USD 26.53 Billion in 2025. The growing inclusion of pasta in plant-based meal kits by foodservice operators and retailers is expanding its B2B relevance, especially as demand for quick, flexitarian-friendly meals continues to gain traction. In turn, the market is expected to grow at a CAGR of 3.34% during the forecast period of 2026-2035 to reach a value of USD 36.85 Billion by 2035.

Growth in the market is also led by rising demand for high-protein, gluten-free, and clean-label alternatives. The market is projected to grow steadily as plant-based ingredients disrupt traditional formulations in the coming years. As per industry reports, in 2023, 6.2 million tonnes of pasta were produced in the European countries, worth EUR 8.9 billion. While the volume was comparable with 2022 (6.1 million tonnes), there was an increase of EUR 1.1 billion in terms of value.

Italy has continued to be the key hub of the global market. According to the pasta market analysis, about 23.5 kg of pasta is consumed by an average Italian per year. Hence, with the growing demand for diverse and innovative pasta across the globe, Italian pasta manufacturers are adopting gluten-free, organic, leguminous, ancient grains, superfoods, and fortified ingredients to improve the nutrition profile of pasta. Further, the United Kingdom’s import substitution strategies are giving rise to domestic pasta brands using British-grown durum wheat.

Moreover, the shift from commodity to curated cuisine has become particularly strong in foodservice and hospitality. Premiumisation, especially within chilled and fresh variants, has resulted in heavy demand in the pasta market, with major chains adopting small-batch, heritage grain pastas to appeal to health-conscious diners. While economic fluctuations pose threats, innovation remains the main focus of the global players.

Base Year

Historical Period

Forecast Period

In 2022, about 6.1 million tons of pasta were produced in the EU.

Italy produces about 3.5 million tons of pasta per annum.

With the rise in gluten intolerance and celiac disease, gluten-free pasta made from alternative grains like quinoa, rice, or corn has become popular.

Compound Annual Growth Rate

3.34%

Value in USD Billion

2026-2035

*this image is indicative*

| Global Pasta Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 26.53 |

| Market Size 2035 | USD Billion | 36.85 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 3.34% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 3.8% |

| CAGR 2026-2035 - Market by Country | India | 3.9% |

| CAGR 2026-2035 - Market by Country | China | 3.6% |

| CAGR 2026-2035 - Market by Type | Chilled/Fresh Pasta | 4.1% |

| CAGR 2026-2035 - Market by Distribution Channel | Online/E-Retailing | 10.3% |

| Market Share by Country 2025 | Saudi Arabia | 1.4% |

The rise in health-conscious consumers has compelled producers to simplify ingredients and eliminate additives. Companies like Garofalo and Banza are investing in clean-label initiatives, offering pasta with three or fewer ingredients. DEFRA's 2024 food innovation roadmap emphasised functional food formulations with traceable, local sourcing. Retailers are onboarding these ranges, boosting the pasta market growth. Additionally, United States-based pasta company Kaizen’s launch of low-carb pasta using lupin flour in May 2022, has sparked attention across B2B buyers seeking keto-compliant SKUs.

Packaging is increasingly becoming a selling point for companies. Compostable and edible pasta wrappers are gaining traction in the European Union, supported by Horizon Europe funding. Brands like F.lli De Cecco are experimenting with seaweed-based biodegradable trays for its fresh pasta line, reducing plastic usage by a significant extent. In the United Kingdom, Waitrose’s aim to switch to 97% recyclable pouches is expected to result in a significant uplift in pasta sales. These shifts offer immense B2B opportunities for co-branding and sustainable supply chain alignment.

Demand for alternative proteins has compelled produces to diversify raw inputs, boosting the pasta market growth. Canada and India are spearheading pulse exports used in legume-based pasta. In addition, the EU’s Common Agricultural Policy for 2023-2027 includes funding schemes supporting crop diversification, which has indirectly benefitted chickpea, lentil, and pea-based pasta categories. Moreover, Barilla offers a red lentil fusilli in partnership with regenerative farms, reinforcing B2B focus on ethical supply chains.

Legacy pasta brands are increasingly embracing Industry 4.0 frameworks to modernise manufacturing, streamline operations and reduce labour bottlenecks, fuelling the pasta market value. In Italy, a notable shift is being witnessed with startups like SmartPasta Design pioneering customisation of raw material formulations and the integration of grain germination and extrusion processes, ensuring consistency in texture, shape and firmness across diverse pasta varieties. Automated systems also enable real-time quality control and predictive maintenance, helping producers lower their operational costs while maintaining artisanal quality. Traditional firms such as Barilla are collaborating with technology suppliers to digitise batch tracking and improve traceability.

The emergence of functional pasta withnin the nutraceutical space is further reshaping the pasta market trends and dynamics. For instance, Nestlé Health Science is trialling vitamin-enriched pasta aimed at elderly consumers across Europe. Additionally, algae-infused pasta with Omega-3 benefits is being tested by United Kingdom-based biotech firm Algagenix, with potential to enter institutional catering via NHS partnerships. This trend, hence, represents a convergence of wellness and daily diet, ideal for public procurement, hospitals, and corporate cafeterias.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The EMR’s report titled “Global Pasta Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

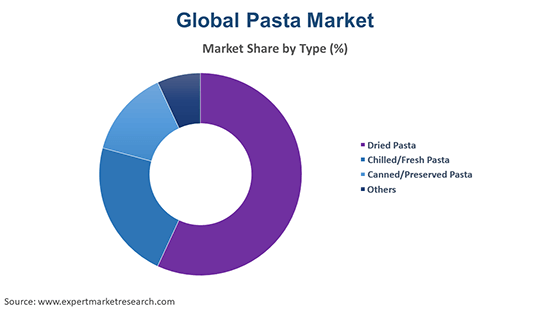

Market Breakup by Type

Key Insight: Dried pasta remains a pantry essential for foodservice due to durability and affordability. Chilled/fresh pasta is gaining premium traction via chefs and upscale retailers seeking quality cues. Canned/preserved pasta caters to institutions, schools, and long-shelf-life retail, often tied with government nutrition schemes. The “others” category including microwave-ready cups and novelty formats, is driven by convenience and impulse-buying.

Market Breakup by Raw Material

Key Insight: Durum wheat holds the dominant position in the global pasta industry, wheat gains popularity among cost-sensitive consumers, and rice supports allergen-free menus. Mixes of quinoa, buckwheat, or multigrain address niche, health-driven consumer demand. Barley and maize derivatives are emerging in nutritionally enhanced formulations. The “others” category includes algae or insect flour-based pastas, which is gaining support from regulatory frameworks.

Market Breakup by Distribution Channel

Key Insight: Supermarkets dominate the market in volume, while online leads in niche penetration, accelerating the pasta market expansion. Convenience stores cater to impulse and ready-to-eat pasta; speciality stores anchor gourmet and regional brands. Other distribution channels include institutional procurement and vending, both reliant on scale and compliance. B2B strategies must match channel strengths with consumer behaviours, pricing models, and logistics capabilities. Omni-channel readiness is becoming a norm for pasta producers seeking sustainable growth.

Market Breakup by Region

Key Insight: Europe with its traditional eating habits and inclination towards innovation, strengthens the pasta demand forecast; North America follows with functional and premium launches. Asia Pacific drives volume growth through localisation. Latin America’s market is value-centric, while Middle East & Africa are driven by urban retail expansion. Each region reflects distinct culinary, regulatory, and logistical realities. Market entry strategies must be tailored, with localisation and agility at their core.

| CAGR 2026-2035 - Market by | Country |

| India | 3.9% |

| China | 3.6% |

| Saudi Arabia | 3.6% |

| Mexico | 3.5% |

| UK | 3.2% |

| USA | 3.1% |

| Canada | XX% |

| France | XX% |

| Italy | XX% |

| Japan | XX% |

| Australia | XX% |

| Brazil | XX% |

| Germany | 2.9% |

By Type, the Dried Pasta Segment Accounts for the Major Share of the Market

Dried pasta continues to dominate the global market due to its extended shelf life, ease of transport, and adaptability across global cuisines. B2B players, especially institutional buyers and foodservice chains, prefer dried pasta for inventory efficiency. Italy and Turkey remain the top exporters, meanwhile India and Egypt have ramped up production owing to subsidised wheat flour policies. Innovations in protein-enriched and high-fibre dried pasta are helping brands expand into health-forward markets. Several EU-backed circular economy projects are exploring upcycled grain integration, offering brands a cost-effective edge. The versatility and price competitiveness make dried pasta a default choice for most of the buyers.

As per the pasta market report, chilled and fresh pasta is fast becoming a premium staple, driven by shifting consumer preferences for texture and freshness. Artisan formats and small-batch processing are trending in upscale B2B supply chains. In 2024, the United Kingdom saw a 6.08% rise in chilled pasta consumption, fuelled by homegrown suppliers leveraging DEFRA’s local food grants. The market also observes a growing traction among meal kit providers like Gousto and HelloFresh, who added chilled pasta lines into their rotating menus.

By Raw Material, Durum Wheat Semolina Registers a Significant Market Share

Durum wheat semolina occupies a significant share in the global market owing to its firm texture and high protein content. The EU’s 2024 Agricultural Reform Strategy has prioritised durum wheat cultivation zones in Southern Europe, ensuring stable raw material flows. As per the pasta industry analysis, Italy alone accounts for over 70% of Europe’s pasta exports. Premium foodservice chains and boutique retailers often demand 100% durum wheat for its cooking performance. Brands like De Cecco and Rummo highlight origin and grind type on packaging to add a layer of provenance as a key selling point.

Rice-based pasta is carving out a niche in the global market for pasta within gluten-free and allergen-sensitive categories. Fuelled by rising intolerance rates and clean-label demands, rice pasta offers a gentle digestive profile and versatility. In 2023, Thai rice exports for processing rose by 12%, while Japan’s Ministry of Agriculture began trials to convert surplus rice into functional pasta products. Brands like Rizopia and Tinkyada are gaining traction among institutional buyers looking for hypoallergenic options in school meals and hospital diets. Technological upgrades in extrusion now allow rice pasta to mimic the al dente texture, which was once exclusive to wheat-based versions.

By Distribution Channel, Supermarkets/Hypermarkets Occupy a Significant Market Share

Supermarkets and hypermarkets continue to boost the pasta market revenue, especially for dried and canned formats. Tesco, Aldi, and Sainsbury’s are actively expanding own-label pasta ranges to include plant-based and fortified offerings. B2B deals for shelf placement are being increasingly dependent on ESG credentials and traceable sourcing. Suppliers are also benefiting from data-sharing arrangements that help tailor SKUs for specific store demographics. With higher turnover and seasonal flexibility, supermarkets offer unmatched visibility for brands that can stand out in a crowded shelf space.

Direct-to-consumer pasta kits, subscription boxes, and health-specific variants are thriving on online platforms like Ocado, Amazon Fresh, and niche organic sites, accelerating the overall pasta consumption. The Great Britain’s online food retail grew by 26.8% in 2025, with pasta among the top search terms. Speciality pasta startups like Pasta Evangelists saw significant growth through digital-only strategies, blending storytelling, convenience, and premium pricing. For B2B players, online channels allow for consumer data mining, targeted promotions, and test marketing without geographic constraints.

By Region, Europe Dominates the Market with the Largest Revenue Share

Dominance of the European market is sustained by Italy, Germany, and France. These countries dominate in terms of production, consumption, and innovation pipelines. Regulatory frameworks such as PDO certification and eco-labelling influence product development. Recent EU funds under the CAP have facilitated the development of artisanal growth in regions like Southern Italy and Eastern Europe. Foodservices in Europe like Zizzi and ASK Italian are witnessing heavy pasta demand, with chefs experimenting with ancient grains and low-GI formats. Institutional buyers are aligning with farm-to-fork initiatives, favouring regional procurement.

The fast-paced growth of the Asia Pacific pasta market is led by changing diets and urbanisation. China, India, and Japan are witnessing strong demand spikes, often for fusion-style and functional pasta. Japan’s convenience-driven retail is embracing chilled and low-calorie noodle-pasta hybrids. Southeast Asia is also witnessing SME-led innovation in cassava and rice-based variants. Multinationals are now localising flavours, textures, and portion sizes to appeal to diverse cultural preferences.

The pasta market players are increasingly focusing on sustainability, premiumisation, and R&D-led differentiation. Automation, eco-packaging, and functional innovation are key areas of focus for the market players. Co-manufacturing, private labelling, and custom formulations for health institutions and gourmet restaurants present ample opportunities for growth. Trends like clean labels, smart manufacturing, plant-based options, sustainable packaging, and fortified pasta are redefining the landscape.

Furthermore, pasta companies are targeting ESG goals via regenerative sourcing and traceability technology. Players are also capitalising on government incentives, like EU’s Horizon grants, to support innovation. Retailer collaborations, subscription models, and vertical integration into farming or packaging have emerged as strategic levers. In addition, blockchain for supply chain transparency, AI-based flavour profiling, and biodegradable pasta wrappers are gaining traction. Firms are also piloting zero-waste production lines, while others explore insect-protein or seaweed-infused pasta formats to meet shifting health and sustainability demands across retail and foodservice.

Founded in 1877, Barilla leads with high-protein, legume-based and carbon-neutral pasta. The company’s innovation centre in Parma focuses on regenerative wheat and AI-powered production lines. Its B2B strategy involves tie-ups with hospitals and universities to deliver nutritional solutions.

Nestlé, established in the year 1866 and based in Switzerland, is innovating through fortified pasta under its Health Science wing, targeting ageing populations. The firm uses smart packaging for freshness and traceability. Nestlé also collaborates with local governments on food security through enriched pasta programmes.

Known for bronze-drawn pasta, F.lli De Cecco di Filippo Fara San Martino S.p.A. emphasises slow-drying processes and non-GMO ingredients. The company founded in 1886, partners with sustainable wheat farmers and has launched eco-packaging pilots supported by EU’s LIFE Programme. De Cecco is also active in HORECA collaborations.

Established in 1937, JSC Makfa leads Eastern Europe in pasta production. The company is integrating AI and robotics into operations and exploring gluten-free innovations using local crops. The firm also supplies bulk pasta to institutional kitchens and military procurement.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Other key players in the market are AGT Food and Ingredients Inc., and General Mills Inc., among others.

Explore the latest trends shaping the global pasta market 2026-2035 with our in-depth report. Gain strategic insights, future forecasts, and key market developments that can help you stay competitive. Download a free sample report or contact our team for customized consultation on pasta market trends 2026.

Australia Pasta and Noodles Market

United States Pasta Market

North America Pasta Market

Iraq Dried Pasta Market

Argentina Pasta Market

Ecuador Pasta Market

Mexico Pasta Market

Indian Pasta Market

Pasta Sauce Market

Vegan Pasta Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

Get in touch with us for a customized solution tailored to your unique requirements and save upto 35%!

In 2025, the pasta market reached an approximate value of USD 26.53 Billion.

The market is projected to grow at a CAGR of 3.34% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach approximately USD 36.85 Billion by 2035.

Key strategies driving the market include exploring new raw materials, co-developing with chefs, leveraging government schemes, adopting AI in production, and aligning with ESG goals.

The key regional markets for pasta are North America, Europe, the Asia Pacific, Latin America and Middle East and Africa.

The raw materials are durum wheat semolina, wheat, mix, barley, rice, maize, and others.

The distribution channels include supermarkets/hypermarkets, convenience stores, speciality stores, online/e-retailing, and others.

The key players in the market include Barilla G. e R. Fratelli S.p, Nestlé S.A, F.lli De Cecco di Filippo Fara San Martino S.p.A., JSC Makfa , AGT Food and Ingredients Inc., and General Mills Inc., among others.

The key challenges are supply chain volatility, price sensitivity, and ingredient regulation.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Raw Material |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Trade Data Analysis |

|

| Price Analysis |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.

Share