Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The global methyl acrylate market attained a value of USD 421.62 Million in 2025. The market is projected to expand at a CAGR of 4.00% through 2035 and set to achieve USD 624.10 Million by 2035. Rising demand for high-performance adhesives and sealants in automotive, packaging and infrastructure sectors is boosting consumption of methyl acrylate-based monomers in formulation-intensive applications.

The industry is currently witnessing rapid technological upgrades as manufacturers push for higher efficiency and tighter quality control across downstream applications. In August 2024, LG Chem announced a breakthrough in its acrylate production line, deploying an advanced polymerization technique that increased yield considerably, enabling faster output for adhesives and coatings used in automotive and packaging applications. This development holds significant implications for the methyl acrylate market, as it directly enhances the production efficiency and quality consistency of acrylate-based formulations.

Across other end-use industries, formulators are turning to methyl acrylate–based monomers to deliver high-performance adhesives, fast-dry coatings and lightweight plastics that align with evolving sustainability standards and stricter regulatory limits on VOCs, boosting the methyl acrylate market opportunities. Manufacturers are responding by launching low-VOC grades, renewable feed-stock alternatives and application-specific copolymers designed for high-volume packaging and automotive markets. For example, in June 2025, Dow Chemical Company introduced low-VOC acrylate products to support regulatory compliance and sustainability goals in Europe.

Base Year

Historical Period

Forecast Period

Compound Annual Growth Rate

4%

Value in USD Million

2026-2035

*this image is indicative*

| Global Methyl Acrylate Market Report Summary | Description | Value |

| Base Year | USD Million | 2025 |

| Historical Period | USD Million | 2019-2025 |

| Forecast Period | USD Million | 2026-2035 |

| Market Size 2025 | USD Million | 421.62 |

| Market Size 2035 | USD Million | 624.10 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 4.00% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 5.2% |

| CAGR 2026-2035 - Market by Country | India | 5.9% |

| CAGR 2026-2035 - Market by Country | China | 5.0% |

| CAGR 2026-2035 - Market by Application | Adhesives and Sealants | 4.5% |

| CAGR 2026-2035 - Market by End Use | Automobile | 4.6% |

| Market Share by Country 2025 | China | 7.8% |

Producers are piloting bio-derived acrylic intermediates and methyl acrylate precursors to reduce cradle-to-gate carbon footprints. LG Chem’s move to commercialize bio-based acrylic acid precursors in February 2025 signals broader interest in fermentative or biomass routes for acrylates, enabling formulators to label low-carbon adhesives and coatings, positively influencing the methyl acrylate market growth avenues. Governments in Europe and Asia are linking incentives to bio-based chemical adoption and providing grants for demo-scale bio-refineries, making early commercial players attractive for long-term offtakes.

Advanced polymerization and process intensification with continuous reactors, better catalysts, process analytics are increasing methyl acrylate yields and lowering specific energy use. Recent industrial upgrades reported by major chemical producers delivered yield improvements, enabling faster throughput for monomer lines used in adhesives and coatings, creating new methyl acrylate industry opportunities. To grow on this, in August 2021, Dow Chemicals launched a methyl acrylate plant of nameplate capacity 50,000 tons at St. Charles in Louisiana in the United States. Energy/regulatory pressure including industrial decarbonization targets and energy efficiency policies, is pushing CAPEX toward smarter plants, where digital process control and PAT (process analytical technology) reduce off-spec production and waste.

End-users in coatings and adhesives are moving to low-VOC and fast-cure formulations where methyl acrylate copolymers offer performance benefits such as tack, adhesion, film formation. Regulatory tightening on VOCs in Europe and North America is incentivizing to switch to reactive/acrylate-based binders and UV-curable systems that reduce solvent loads, redefining the methyl acrylate market dynamics. For example, in July 2024, Arkema achieved ISCC-PLUS mass-balance certification at its acrylic monomers facility in Clear Lake, Texas, enabling the production of bio-attributed specialty acrylic monomers, including methyl acrylate-based copolymers, aimed at low-VOC, fast-cure coatings and adhesives for new mobility and building efficiency applications.

Producers are moving beyond commodity supply toward collaborative development. Co-developing copolymers, custom monomer blends and application trials with adhesive and packaging manufacturers are all part of this emerging methyl acrylate market trend. This vertical cooperation reduces time-to-market for innovative adhesives and packaging films, and locks in offtake through technical services and joint IP. For example, in April 2024, BASF SE signed a Letter of Intent with Youyi Group to supply acrylates (butyl/acrylates) from its Zhanjiang site, aligned with Youyi’s new BOPP film-and-tape facility in Guangdong.

Rapid capacity additions in Asia mainly in China, India, Korea, are making regional supply more responsive and price-competitive, while Western producers focus on specialty grades and sustainability certifications. In January 2023, BASF inaugurated a new production complex at its Verbund site in Zhanjiang, China, responding to the rising demand in the methyl acrylate market. That geographic split is encouraging long-term procurement strategies such as regional sourcing for commodity grades and localized contracts for specialty, low-VOC or bio-based monomers.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The EMR’s report titled “Global Methyl Acrylate Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Application

Key Insight: The methyl acrylate industry report delves into several applications including surface coatings, adhesives, plastic additives, detergents, textiles and specialty chemical syntheses. Coatings need weathering resistance and fast cure, whereas adhesives demand tack and low-VOC profiles, plastic additives require compatibility with polyolefins and performance at process temperatures. Textiles and detergents need precise copolymer properties. Suppliers are therefore offering commodity MA for large-volume polymer producers and technical, low-impurity or bio-derived grades for formulation-intensive sectors.

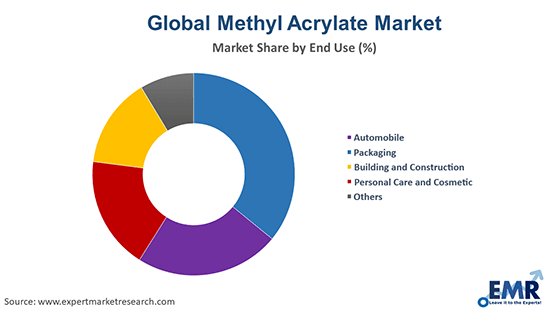

Market Breakup by End Use

Key Insight: End use categories include packaging, automotive, construction, personal care and others. Packaging drives volume via adhesives and coatings. Automotive applications are rapidly growing their shares in the market with electrification and polymer substitution needs. Construction uses acrylate-based sealants and coatings for durability, whereas personal care leverages specialty copolymers for film formers. Each end-use demands distinct monomer attributes including purity, residuals, reactivity, pushing suppliers to offer certified grades, technical support, and co-development services.

Market Breakup by Region

Key Insight: The regional methyl acrylate market dynamics suggest that Asia Pacific supplies scale and cost-competitive commodity methyl acrylate. Europe and North America are value-led markets prioritizing low-VOC, bio-based and high-purity grades. Latin America and MEA are emerging demand centers tied to construction and packaging growth. Strategic tolling, local partnerships and long-term offtake agreements are becoming standard to manage price volatility and quality assurance.

| CAGR 2026-2035 - Market by | Region |

| Asia Pacific | 5.2% |

| North America | 3.9% |

| Europe | XX% |

| Latin America | XX% |

| Middle East and Africa | XX% |

By application, technical/high-purity grades dominate the market because purity drives formulation performance

Surface coatings remain the largest application as methyl acrylate monomers underpin acrylic and copolymer binders used in architectural, industrial and UV-curable coatings. MA-based monomers enable fast film formation, low-temperature cure, critical for high-performance protective and decorative systems. Coating formulators are adopting specialized methyl acrylate grades that reduce yellowing and improve weathering when copolymerized with butyl or ethyl acrylates. For example, Panacol offers a two-component high-performance structural adhesive in its product range, called Penloc GTN to process methyl acrylate based low-odor formulations. Regulatory VOC caps and demand for durable, fast-curing coatings in infrastructure projects are driving formulators toward acrylate chemistries. Suppliers are providing application labs, scale-up trials, and certified low-impurity monomers to accelerate adoption in OEM and industrial coatings.

| CAGR 2026-2035 - Market by | Application |

| Adhesives and Sealants | 4.5% |

| Surface Coatings | 4.2% |

| Chemical Synthesis | XX% |

| Plastic Additives | XX% |

| Detergents | XX% |

| Others | XX% |

Adhesives and sealants are expanding rapidly their methyl acrylate market shares as packaging, automotive and construction sectors demand high-performance, fast-cure, and low-VOC adhesives. Methyl acrylate is a key monomer for pressure-sensitive adhesives, hot-melt emulsions, and UV-reactive systems that require tack, peel strength and environmental resistance. Formulators are increasingly using MA-rich copolymers to replace solvent-borne systems, enabling VOC reductions while maintaining bond performance. Companies are launching tailored MA grades optimized for PSA performance or hot-melt processing, and collaborating with OEMs on pilot runs.

By end use, packaging leads the market due to high output and surging adhesive demand

Packaging is the dominant end-use because methyl acrylate–based adhesives and coatings deliver rapid set times, strong bonds, and compatibility with high-speed converting lines. Food-contact packaging trends such as lightweight films, recyclable mono-materials are pushing formulators toward acrylic adhesives that enable heat-sealing and high-speed lamination while meeting migration and safety criteria. MA copolymers provide balance between tack, peel strength and temperature resistance required for flexible packaging and pressure-sensitive labels.

| CAGR 2026-2035 - Market by | End Use |

| Automobile | 4.6% |

| Packaging | 4.3% |

| Building and Construction | XX% |

| Personal Care and Cosmetic | XX% |

| Others | XX% |

Automotive end use drives fast-paced methyl acrylate market growth as lightweighting and assembly efficiency require advanced adhesives and coatings. Methyl acrylate–based monomers have become important in primeless bonding, structural adhesives and protective coatings. In September 2025, The Mitsubishi Chemical Group declared that it is collaborating with Honda Motor Co., Ltd. to develop PMMA polymethyl methacrylate materials for automotive body components. Electrification and increased use of polymers in interiors create demand for adhesives with thermal stability, low VOCs, and long shelf life. MA-derived copolymers are being tailored for bonding plastics to metals, vibration damping, and UV-resistant exterior coatings.

Asia Pacific dominates the global industry driven by capacity expansion and lower costs

Asia Pacific leads the global industry due to integrated petrochemical complexes, rising packaging manufacturing, and strong coatings demand. Investments in acrylics complexes, namely acrylic acid, butyl/acrylates across China, Korea and India are improving regional self-sufficiency and lowering lead times for converters. Local capacity expansion is driven by downstream packaging and automotive supply chains relocating or expanding regionally.

The methyl acrylate market expansion in Europe is growing on a value basis as regulatory pressure, VOC limits and circularity policy incentivize premium and bio-derived monomers. European programs and funding mechanisms for low-carbon chemicals are encouraging investments in renewable feedstocks and process electrification. This is prompting producers to commercialize low-impurity MA grades, bio-AA derivatives and higher-value copolymers for specialized adhesives and coatings.

| CAGR 2026-2035 - Market by | Country |

| India | 5.9% |

| China | 5.0% |

| Brazil | 4.6% |

| USA | 3.9% |

| Australia | 3.5% |

| Canada | XX% |

| UK | XX% |

| Germany | XX% |

| France | 3.5% |

| Italy | XX% |

| Japan | XX% |

| Saudi Arabia | XX% |

| Mexico | XX% |

Methyl acrylate companies are prioritizing process intensification, deploying continuous polymerization, advanced catalysts and digital process control to lift yields and reduce energy use, improving margins in a commodity market. Simultaneously, investment in bio-based acrylic precursors, low-VOC monomer grades and regional satellite plants is bringing supply closer to converters in packaging, adhesives and automotive sectors.

Downstream partnerships for co-development of tailored copolymers and pilot trials are locking in offtake and shortening innovation cycles. New pricing benchmarks and spot trading platforms are increasing transparency while exposing smaller players to volatility. For methyl acrylate market players, opportunities lie in securing long-term contracts, engaging in tolling arrangements, and procuring certified low-carbon grades. Competitive advantage is anticipated to stem from combining scale economics with application expertise and verified sustainability credentials.

Arkema SA was established in 2004 and is headquartered in La Défense, France. The firm is focusing on specialty acrylates and advanced monomer technologies serving coatings, adhesives and high performance plastics. Arkema is commercializing low VOC acrylate grades and investing in bio-based acrylic precursors to meet sustainability mandates.

LG Chem Ltd. was established in 2009 and is headquartered in Seoul, South Korea. LG Chem is leveraging advanced polymerization techniques and expanded acrylate capacity to serve adhesives, coatings and electronics markets. The company is commercializing higher yield production routes and low impurity methyl acrylate grades for fast cure systems.

BASF SE was established in 1865 and is headquartered in Ludwigshafen, Germany. The company is focusing on integrated acrylics platforms and specialty monomer formulations for high performance coatings and industrial adhesives. BASF is advancing catalyst technologies and process analytics to boost methyl acrylate throughput while reducing emissions.

Shanghai Huayi Acrylic Acid Co., Ltd. was established in 1993 and is headquartered in Shanghai, China. It is focusing on acrylic monomers including methyl acrylate and acrylic acid for domestic coatings, adhesives and polymer markets. The company is enhancing purification lines and investing in automated QA to produce low-impurity grades suited to formulation-sensitive applications.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Other key players in the methyl acrylate market report include Nippon Shokubai Co., Ltd., and SIBUR International GmbH, and others.

Unlock the latest insights with our methyl acrylate market trends 2026 report. Discover regional growth patterns, consumer preferences, and key industry players. Stay ahead of competition with trusted data and expert analysis. Download your free sample report today and drive informed decisions in the market.

Upto 15% Off

USD

$3999 $3599

$2499 $2249

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

Get in touch with us for a customized solution tailored to your unique requirements and save upto 35%!

The market is projected to grow at a CAGR of 4.00% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach about USD 624.10 Million by 2035.

Companies are investing in bio-feedstock routes, upgrading to continuous processes, forming co-development partnerships, expanding regional satellite plants, and securing long-term offtake and tolling agreements globally.

The rising demand for methyl acrylate in the packaging sector, the growing demand for surface coatings, and the increasing use of the chemical in water treatment are the key trends supporting the market development.

The major regions in the market are North America, Latin America, the Middle East and Africa, Europe, and the Asia Pacific.

Surface coatings, chemical synthesis, adhesives and sealants, plastic additives, detergents, and textiles, among others, are the major applications of methyl acrylate.

The various end uses of methyl acrylate include automobile, packaging, building and construction, and personal care and cosmetics, among others.

The key players in the market include Arkema SA, LG Chem Ltd., BASF SE, Shanghai Huayi Acrylic Acid Co., Ltd., Nippon Shokubai Co., Ltd., and SIBUR International GmbH, among others.

In 2025, the market reached an approximate value of USD 421.62 Million.

Volatile feedstock prices, strict VOC and safety regulations, high CAPEX for bio and process upgrades, supply chain disruptions, and quality consistency demands are constraining margins and growth opportunities for producers.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Application |

|

| Breakup by End Use |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.

Share