Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The global liquid eggs market was valued at USD 13.92 Billion in 2025. The market is expected to grow at a CAGR of 5.90% during the forecast period of 2026-2035 to reach a value of USD 24.69 Billion by 2035. Rising demand for high-protein functional foods is boosting liquid egg innovation across nutraceuticals and ready-to-drink beverages, positioning it as a versatile ingredient beyond traditional culinary applications.

The rising institutional demand from foodservice and bakery chains is one of the major growth motivators of the market. Quick-service restaurants (QSRs) and catering companies increasingly prefer liquid eggs over shell eggs for better food safety compliance and efficiency. According to the liquid eggs market analysis, 11% of eggs produced in the United States go to egg breaking, resulting in 2.9 x 10 kg (6.40 x 10 Ibs) of liquid egg products, per day.

Moreover, the rise of automation in liquid egg processing is equally reshaping industry efficiency. Companies are investing in advanced pasteurization lines and packaging systems to enhance hygiene standards and extend usability. With government-backed sustainability pledges and food safety regulations converging, the market is no longer about basic replacement of shell eggs, it is becoming a technology-driven sector critical to industrial food supply networks.

Base Year

Historical Period

Forecast Period

Compound Annual Growth Rate

5.9%

Value in USD Billion

2026-2035

*this image is indicative*

Large-scale bakeries, cafeterias, and QSR operators are driving liquid egg demand due to reduced preparation time and consistent quality. McDonald’s, for instance, uses liquid eggs in select menus to maintain uniformity across stores. Governments mandating stricter food safety audits, especially post-pandemic, reinforce the case for liquid eggs over shell eggs in institutional use. This liquid eggs market trend highlights how efficiency, safety, and scalability are the cornerstones of demand among high-volume buyers.

The transition to cage-free systems is directly influencing the global industry. The European Commission’s cage-free commitment by 2023 has already prompted large suppliers like Cal-Maine Foods to expand cage-free liquid egg lines. Major retailers, including Walmart and Tesco, have introduced supplier guidelines favoring cage-free liquid eggs. This creates a demand in the liquid eggs market as they serve as the preferred processed form of cage-free eggs for manufacturers. By aligning with policy targets, liquid egg producers not only tap into ethical sourcing trends but also secure long-term procurement contracts.

Countries with advanced processing infrastructure are increasing exports of liquid eggs to regions with limited production. For instance, the Netherlands exported over 415,000 tons of liquid eggs in 2020 catering to demand in Germany and the United Kingdom. Trade liberalization policies and food security partnerships in Asia Pacific are further widening the scope for liquid eggs market expansion. This allows producers to capture international contracts, especially from emerging economies where bakery and confectionery industries are scaling quickly but lack local processing capacity.

Innovation in pasteurization and aseptic packaging is transforming shelf stability for liquid eggs. Companies like Pulviver are adopting ultra-high temperature (UHT) processing to extend shelf life to 90 days without compromising nutrition. These liquid eggs market developments are not just about longer storage, they also open up new distribution channels such as e-commerce and long-haul exports, making liquid eggs more viable in regions with less cold chain infrastructure.

Liquid eggs consumption is moving beyond traditional baking and foodservice into the nutraceutical and functional beverage space. Start-ups are experimenting with protein shakes and fortified drinks using liquid egg whites due to their clean-label protein profile. Government nutrition programs that promote high-protein diets in schools and elderly care are also indirectly fueling this adoption, placing liquid eggs as a central ingredient in future protein innovation.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The EMR’s report titled “Global Liquid Eggs Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Source

Key Insight: The source-based categorization of the liquid eggs market report reflects two parallel growth tracks. Cage-free formats lead to premium and regulatory-compliant adoption, while conventional forms sustain demand in cost-sensitive regions. Collectively, they ensure both ethical and scalable supply channels remain integral to the market’s overall growth.

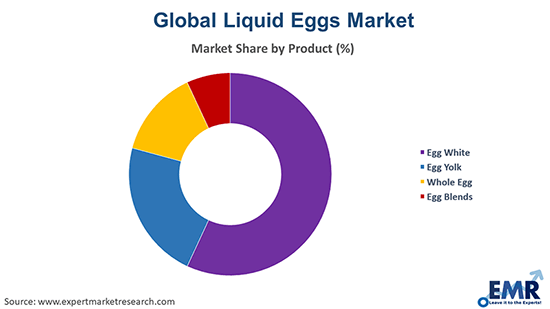

Market Breakup by Product

Key Insight: Egg whites dominate the global market, propelled by rising demand for protein-focused innovation, while egg blends record fast growth owing to their adaptability in industrial use. At the same time, yolks and whole eggs maintain relevance across traditional bakery, confectionery, and broader culinary applications, ensuring the category secures adoption across diverse food industries.

Market Breakup by Type

Key Insight: Frozen liquid eggs continue to dominate the market, supported by their long shelf stability, cost-effectiveness, and strong suitability for exports. These formats are especially favored by large bakeries and international distributors managing bulk demand in the liquid eggs market. Meanwhile, refrigerated liquid eggs are recording rapid growth, appealing to buyers who prioritize freshness and quick preparation. Their adoption is expanding in foodservice outlets and retail chains, aligning with urban consumer preferences and just-in-time production models in dynamic, convenience-driven markets.

Market Breakup by Packaging

Key Insight: Packaging trends in the liquid eggs market underscore how plastic pouches maintain cost-driven leadership, while carton boxes gain traction with sustainability-focused buyers. PET bottles and other niche formats continue supporting specialized needs, especially in retail-ready and premium product categories.

Market Breakup by Distribution Channel

Key Insight: Supermarkets and hypermarkets remain the dominant distribution channels, supported by their broad accessibility and consistent supply networks. In contrast, online platforms are driving rapid growth by offering digital convenience. Meanwhile, specialty stores, convenience outlets, and other niche formats continue to serve regional demands and targeted sourcing requirements, ensuring the market remains diverse and adaptive across different buyer categories.

Market Breakup by End Use

Key Insight: Food and beverages remain the central pillar of end-use demand, whereas dietary supplements are accelerating with protein-led innovation. At the same time, pharmaceuticals, cosmetics, animal feed, and niche applications sustain consistent roles, drawing on the functional and nutritional strengths of liquid eggs.

Market Breakup by Region

Key Insight: Regionally, North America substantially contributes to the liquid eggs market value with structured supply chains and food safety emphasis, while Asia Pacific drives growth through foodservice expansion. Europe, Latin America, and the Middle East & Africa each add regional momentum based on regulatory, demographic, and industrial consumption factors.

By source, cage-free liquid eggs emerge as the largest shareholder owing to ethical farming transition

Cage-free liquid eggs dominate the market as governments, retailers, and food manufacturers commit to animal welfare standards. Foodservice giants like Starbucks have committed to 100% cage-free eggs globally, accelerating processing demand. As cage-free shell eggs move through supply chains, the liquid egg format becomes the logical choice for commercial use, particularly in bakery and confectionery industries where bulk handling is required, strengthening the liquid eggs demand forecast.

Despite the cage-free shift, conventional liquid eggs continue to record rapid consumption rates due to affordability and availability. In regions like Asia-Pacific and Latin America, where price sensitivity dominates, conventional eggs supply the largest portion of liquid egg manufacturing. Small- and medium-sized bakeries often prioritize cost efficiency over sourcing standards, which fuels conventional egg processing. In addition, government-backed food distribution schemes in lower-income economies often rely on conventional formats due to their scalability and lower procurement costs.

By product, egg white liquid formats account for the dominant share driven by protein-centric applications

Liquid egg whites dominate the product category owing to their high protein content and versatility. They are widely used in protein supplements, ready-to-drink beverages, and sports nutrition products. Commercial bakeries also prefer liquid egg whites for meringues, confectionery fillings, and gluten-free innovations. The surge in consumer demand for clean-label protein and allergen-friendly options has further propelled egg whites to lead the liquid eggs market globally, with both B2B manufacturers and end-users embracing their functional and nutritional benefits.

Liquid egg blends which include combinations of whole eggs, yolks, or whites with stabilizers, are growing at the fastest pace due to their adaptability. Large-scale bakeries, sauce manufacturers, and catering services prefer blends for consistent functionality, better texture, and extended shelf stability. For example, custom liquid egg blends are being adopted by frozen meal producers in Europe to standardize product formulations. With demand expanding across ready-to-eat and processed foods, liquid egg blends are emerging as the go-to option for manufacturers needing flexibility in production.

By type, frozen liquid eggs secure the largest share due to longer shelf stability

The continuous dominance of frozen liquid eggs is primarily because of their extended shelf life and suitability for bulk distribution. Large-scale bakeries, catering firms, and institutional food suppliers prefer frozen formats since they allow efficient inventory management while minimizing spoilage. Frozen liquid eggs are often used in high-volume production where seasonal demand must be met without compromising food safety or functionality. Their ability to withstand longer transportation cycles also makes them highly attractive for export-driven companies.

Refrigerated liquid eggs are witnessing the fastest growth in the liquid eggs market, supported by increasing demand for freshness and shorter preparation times in foodservice sectors. Restaurants, cafes, and small bakeries often prefer refrigerated variants because of their ready-to-use nature and better preservation of natural taste. The format appeals strongly to urban buyers who value quick turnaround and clean-label ingredients.

By packaging, plastic pouches account for a substantial market share due to cost efficiency

Plastic pouch packaging dominates the liquid eggs market due to its lightweight structure, ease of handling, and affordability for both producers and buyers. Pouches are widely adopted in institutional kitchens and bakeries as they reduce packaging costs while offering adequate protection for short- to medium-term storage. They also appeal to logistics chains that prioritize flexible and stackable packaging formats.

Carton-based packaging is emerging as the fastest-growing format, backed by rising sustainability targets and customer demand for eco-friendly solutions. Cartons provide superior branding opportunities, allowing suppliers to communicate product quality, sourcing standards, or cage-free certifications directly on packaging. This makes them a preferred choice for premium products targeting foodservice chains and retail buyers, thereby accelerating liquid eggs consumption. Their recyclability and lightweight design resonate strongly with environmentally conscious companies, especially in Europe and North America where green packaging regulations are tightening.

By distribution channel, hypermarkets and supermarkets capture substantial market share owing to wide accessibility

Hypermarkets and supermarkets remain the dominant distribution channel, given their large-scale presence and ability to offer variety under one roof. Bulk buyers, including restaurants and bakeries, often procure liquid eggs through these outlets due to consistent availability and competitive pricing. Retail shelf presence also boosts visibility, helping manufacturers reach both B2B and B2C customers simultaneously. The widespread distribution network of supermarket chains further supports efficient regional supply of liquid eggs.

As per the liquid eggs industry report, online channels are recording the fastest growth, supported by digitalization of food procurement and the rise of B2B marketplaces. Large institutional buyers are increasingly sourcing through e-commerce platforms and digital procurement portals, ensuring cost transparency and streamlined supply chains. Online distribution also caters to smaller restaurants and catering firms, giving them direct access to liquid egg suppliers without intermediary costs.

By end use, food and beverages clock in the largest share of the market due to industrial usage

Food and beverages largely contribute to the liquid eggs demand growth, supported by their indispensable role in bakery, confectionery, and foodservice industries. Large-scale bakeries rely heavily on liquid egg formats for consistent quality in cakes, pastries, and sauces, while QSR chains use them for speed and food safety assurance. The convenience of liquid eggs reduces labor costs and preparation time in high-volume kitchens. Furthermore, the rising demand for protein-enriched bakery goods and functional food products strengthens their application.

Dietary supplements are emerging as the fastest-growing end-use category, boosting the liquid eggs market revenue, fueled by the increasing consumer demand for clean-label, high-protein, and functional nutrition. Liquid egg whites, in particular, are finding strong adoption in protein powders, shakes, and functional beverages. Start-ups and nutraceutical brands are incorporating egg proteins due to their digestibility and complete amino acid profile, positioning them as a natural alternative to whey.

North America captures the dominant position in the market owing to structured supply chains

North America leads the global market due to its advanced processing infrastructure, strong demand from foodservice industries, and regulatory focus on food safety. The United States is home to some of the largest integrated egg processors globally, ensuring reliable supply to QSR chains, bakeries, and institutional buyers. The region also benefits from early adoption of cage-free commitments, which accelerates the shift toward liquid egg processing. Demand in the liquid eggs market is amplified by the well-established retail ecosystem and growing consumer preference for protein-enriched products.

The fast-paced growth of the Asia Pacific market is supported by the rapid expansion of bakery, confectionery, and foodservice industries in countries like China, India, and Japan. Rising disposable incomes and urbanization have boosted demand for convenient and high-protein food formats, pushing the adoption of liquid eggs across both B2B and retail sectors. Additionally, local producers are increasingly investing in modern processing plants to cater to growing institutional consumption.

The global industry is becoming increasingly competitive as players shift focus toward sustainability, product innovation, and efficient distribution. Liquid egg companies are exploring opportunities in nutraceutical applications, aseptic packaging, and cage-free liquid formats to align with evolving consumer and regulatory expectations. There is also rising emphasis on digital procurement channels, enabling manufacturers to reach institutional buyers directly while lowering costs.

Liquid eggs market players also find opportunities in high-protein functional foods, ready-to-drink beverages, and export markets where demand for processed egg products is growing rapidly. With foodservice and bakery industries scaling globally, companies that prioritize traceability, food safety compliance, and customized product formulations are best positioned to gain long-term advantage.

Nature-Egg LLP, established in 2015 and headquartered in Uttar Pradesh, India, specializes in supplying pasteurized liquid eggs for industrial bakeries and hotels. The company focuses on cage-free and high-protein formulations, positioning itself as a sustainable player with strong regional distribution networks.

Cargill Incorporated, founded in 1865 with headquarters in the United States, is a global leader in agricultural and food processing. It caters to the liquid eggs market by offering large-scale processing capacity, aseptic packaging solutions, and advanced food safety compliance systems for multinational clients.

Nest Fresh Eggs Inc., established in 1991 and based in Colorado, United States, focuses on cage-free and organic egg solutions. The company supplies liquid eggs primarily to foodservice chains and institutional buyers while promoting humane sourcing and transparent supply chain practices.

Global Food Group, headquartered in Netherlands and founded in 1959, specializes in supplying egg-based liquid and powdered products across Europe. Its strength lies in innovation, with investments in spray-drying and custom egg blends tailored for bakery, confectionery, and protein drink manufacturers.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Other key players in the market are Bumble Hole Foods Limited, Noble Foods Company, Ovostar LTD, among others.

Explore the latest trends shaping the global liquid eggs market 2026-2035 with our in-depth report. Gain strategic insights, future forecasts, and key market developments that can help you stay competitive. Download a free sample report or contact our team for customized consultation on liquid eggs market trends 2026.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

Get in touch with us for a customized solution tailored to your unique requirements and save upto 35%!

In 2025, the liquid eggs market reached an approximate value of USD 13.92 Billion.

The market is projected to grow at a CAGR of 5.90% between 2026 and 2035.

Companies are investing in automation, expanding cage-free lines, exploring functional food partnerships, improving cold chain networks, and leveraging digital sales platforms to strengthen their position in the liquid eggs market.

The key trends of the market include the shift from the purchase of shelled eggs to liquid eggs, along with the major companies in the market increasing their liquid egg production capacity.

The major regional markets of liquid eggs are North America, Europe, and the Asia Pacific, Latin America, and the Middle East and Africa.

The major sources of the product are cage-free and conventional.

The leading types of liquid eggs in the market are frozen and refrigerated.

The major products in the liquid eggs industry are egg white, egg yolk, whole egg, and egg blends.

The significant packaging in the market are plastic pouches, carton boxes, and PET bottles, among others.

The major distribution channels of the products are hypermarkets and supermarkets, convenience stores, specialty stores, and online, among others.

The significant end-use sectors of the product in the market are food and beverages, pharmaceuticals, cosmetics and personal care, dietary supplements, and animal feed, among others.

The key players in the market include Nature-Egg LLP, Cargill Incorporated, Nest Fresh Eggs Inc., Global Food Group, Bumble Hole Foods Limited, Noble Foods Company, Ovostar LTD, among others.

Rising feed costs, regulatory pressure on cage-free sourcing, and intense price competition are the key challenges companies face while maintaining profitability in the liquid eggs market.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Source |

|

| Breakup by Product |

|

| Breakup by Type |

|

| Breakup by Packaging |

|

| Breakup by Distribution Channel |

|

| Breakup by End Use |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.

Share