Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The global in vitro diagnostics market was valued at USD 81.78 Billion in 2024, driven by the increasing demand for advanced diagnostic facilities across the globe. The market is anticipated to grow at a CAGR of 6.20% during the forecast period of 2025-2034 to achieve a value of USD 149.24 Billion by 2034.

Base Year

Historical Year

Forecast Year

Value in USD Billion

2025-2034

In-Vitro Diagnostics Market Outlook

*this image is indicative*

The in vitro diagnostics (IVD) market is experiencing significant momentum, driven by continuous innovations and a rising global burden of chronic diseases and infectious diseases. These factors are fuelling diagnostic market growth, as the demand for accurate, timely, and non-invasive diagnostic procedures intensifies. Increasing adoption of point-of-care testing and automated analyzers in both hospitals and clinical laboratories has made diagnostic processes more efficient and accessible, enabling quicker early disease detection and better disease management. Healthcare systems worldwide are increasingly integrating IVD technologies to support personalized medicine, aiming to tailor treatments for individual patients based on specific biomarkers and disease profiles.

Moreover, the shift towards prevention strategies is prompting healthcare providers to rely more heavily on diagnostic testing to identify risks before symptoms emerge, thereby improving patient outcomes. From monitoring blood glucose levels to screening for cancer and infectious agents, IVD is a cornerstone of modern medicine. The convergence of digital health tools with diagnostics is also enhancing data interpretation and care decisions. As the demand for cost-effective and efficient testing solutions continues to rise, the in vitro diagnostics market is poised for strong growth, offering substantial opportunities for innovation and transformation across the global healthcare landscape.

DRIVER: Rising Elderly Population Driving Chronic and Infectious Disease Prevalence

The growing global geriatric population significantly contributes to the rising incidence of chronic and infectious diseases, thereby driving demand for in vitro diagnostics (IVD). Ageing individuals are more prone to conditions such as diabetes, cancer, cardiovascular, and respiratory disorders, all requiring continuous monitoring and early detection. For instance, in January 2025, Beckman Coulter Diagnostics launched new Research Use Only (RUO) blood-based biomarker immunoassays for neurodegenerative disease research, targeting p-Tau217, GFAP, NfL, and APOE ε4, crucial biomarkers for advancing age-related diagnostics. With immunosenescence increasing infection risks, precise diagnostic tools are essential. This surge in demand, supported by healthcare awareness and accessibility, reinforces IVD technologies' role in personalised, preventive care across ageing populations.

RESTRAINT: Limited Reimbursement Structures Hindering Market Expansion

One of the primary constraints affecting the IVD market is the presence of unfavourable reimbursement policies across several regions. Many healthcare systems lack comprehensive coverage for advanced diagnostic tests, including molecular diagnostics and genetic testing, limiting patient access and reducing the incentive for providers to adopt such technologies. As a result, despite innovations in IVD technologies, uptake may remain subdued due to affordability concerns. In low and middle-income regions, reimbursement challenges are even more pronounced, affecting investments in clinical laboratories and discouraging widespread deployment of automated analyzers or point-of-care testing. Inconsistent policy frameworks, varying payer perspectives on test necessity, and frequent delays in approval for coverage further compound the issue. This regulatory and financial uncertainty acts as a barrier to diagnostic market growth, particularly for tests that are essential in early detection and personalised medicine. Addressing these limitations through policy reform and broader reimbursement inclusion is crucial to realising the full potential of in vitro diagnostics in enhancing patient outcomes and reducing long-term treatment costs.

OPPORTUNITY: Untapped Potential in Developing Regions Boosting Future Growth

The market is witnessing lucrative expansion possibilities in emerging markets due to rising healthcare expenditure, improved diagnostic infrastructure, and growing awareness of non-invasive diagnostic procedures. Countries across Asia Pacific, Latin America, and Middle East and Africa are seeing increased demand for point-of-care testing, driven by high rates of infectious and chronic diseases. For instance, in January 2025, GHIT Fund invested USD 4.2 million in developing a leishmaniasis diagnostic tool, highlighting such global efforts. Government-led health screening programmes and growing collaborations between global firms and local providers enhance diagnostic access in underserved areas. These regions also benefit from mobile diagnostics, digital health solutions, and growing clinical laboratory capacity. The focus on personalised medicine and IVD technologies tailored to regional health needs is fostering inclusive, sustainable market growth.

CHALLENGE: Operational Complexities Creating Market Limitations

Despite rapid technological advancements, the IVD market faces notable operational barriers that impede widespread adoption. Challenges include high equipment costs, the need for skilled technicians, strict regulatory compliance, and complex sample handling protocols, especially in decentralised settings. Healthcare providers in smaller clinics or rural locations may lack the necessary infrastructure to deploy advanced IVD technologies or maintain automated analyzers, leading to delays in test results or limited access. Integration with electronic health records, interoperability issues, and quality assurance compliance further complicate implementation. These operational hurdles restrict the market’s ability to fully capitalise on innovations in early disease detection, especially in homecare or resource-limited settings, and must be addressed for long-term scalability.

The global in vitro diagnostics (IVD) market ecosystem is shaped by a complex network of diagnostic developers, laboratory service providers, healthcare institutions, and regulatory authorities. This ecosystem functions collaboratively to ensure timely diagnosis, effective disease management, and patient-centric care. Technological advancements, increased awareness of personalised medicine, and rising disease prevalence continue to strengthen this network. The adoption of automated systems and digital connectivity is further streamlining workflows, optimising testing efficiency, and enabling faster clinical decisions across diverse healthcare settings.

Blood, Serum, and Plasma Samples to Dominate the IVD Specimen Segment

Blood, serum, and plasma emerged as the most commonly used specimens in the in vitro diagnostics industry due to their high reliability and ease of collection. These biological samples allow accurate assessment of a wide range of diseases including infectious, metabolic, and autoimmune disorders. Their compatibility with various diagnostic platforms, such as immunoassays and molecular tests, makes them highly suitable for both routine screenings and advanced investigations. The segment’s dominance is also driven by the increasing demand for non-invasive testing, rising prevalence of chronic conditions, and continuous advancements in biomarker-based diagnostics.

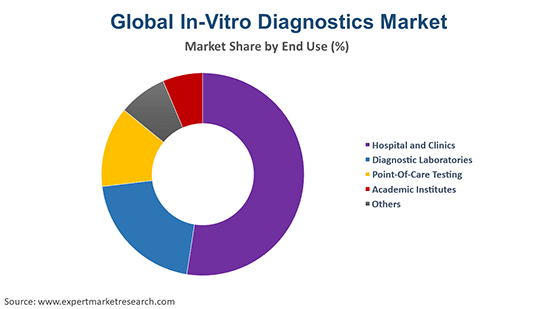

Hospitals and Clinics to Lead the End Users Segment of IVD Solutions

Hospitals and clinics held the largest market share in the IVD sector, as they serve as the primary centres for patient diagnosis, monitoring, and treatment. Their extensive infrastructure, access to trained personnel, and investment capacity enable large-scale deployment of automated IVD systems and high-throughput testing. These facilities also play a critical role in managing acute and chronic diseases through early detection and ongoing disease management. With increasing patient volumes and demand for rapid diagnostics, hospitals and clinics continue to drive growth in the global IVD market.

North America is set to account for the largest share of the global in vitro diagnostics (IVD) market due to its well-established healthcare infrastructure, high healthcare spending, and early adoption of advanced IVD technologies. The region benefits from widespread access to point-of-care testing, growing awareness of personalized medicine, and rising prevalence of chronic and infectious diseases. Furthermore, the presence of major market players and ongoing investments in diagnostic innovation support continued market dominance. Government initiatives promoting early disease detection and prevention strategies also contribute significantly. The robust network of clinical laboratories and strong regulatory frameworks further bolster the region’s leadership in the global IVD industry.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

In-Vitro Diagnostics Market Report and Forecast 2025-2034 offers a detailed analysis of the market based on the following segments:

By Product

By Specimen

By Techniques

By Application

By Test Location

By End User

By Region

The key features of the market report comprise patent analysis, grants analysis, funding and investment analysis, and strategic initiatives by the leading players. The major companies in the market are as follows:

Abbott, headquartered in Illinois, USA, is a global leader in in vitro diagnostics (IVD), offering a wide range of diagnostic tools, including point-of-care testing and laboratory-based analyzers. The company’s innovative diagnostic solutions support early disease detection and chronic disease management, enhancing patient outcomes. Abbott’s strong global presence and continuous R&D investments drive market competitiveness.

Based in Massachusetts, USA, Thermo Fisher Scientific is a key player in the IVD market, offering advanced diagnostic instruments, reagents, and software. Its comprehensive portfolio supports clinical laboratories in delivering precise diagnostics across infectious diseases and oncology. With ongoing innovation and strategic acquisitions, the company plays a critical role in expanding access to personalised diagnostic solutions worldwide.

Roche Diagnostics, a division of Switzerland-based F. Hoffmann-La Roche AG, is a leading provider of IVD technologies. Renowned for its molecular diagnostics and automated analyzers, Roche supports accurate disease detection and treatment monitoring. The company’s strong presence in clinical laboratories and commitment to personalised healthcare positions it at the forefront of diagnostic market growth.

Danaher Corporation, headquartered in Washington, D.C., owns several major diagnostics companies including Beckman Coulter and Cepheid. It offers cutting-edge solutions across molecular, clinical, and microbiology diagnostics. Danaher’s strong innovation pipeline and focus on digital diagnostics contribute to efficient disease detection and improved healthcare delivery, strengthening its footprint in the global IVD market.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Other key players in the market include BIOMÉRIEUX, Becton, Dickinson and Company, QIAGEN, Quidel Corporation, Quest Diagnostics Incorporated and Siemens Healthineers AG.

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

Get in touch with us for a customized solution tailored to your unique requirements and save upto 35%!

The global in vitro diagnostics market was valued at USD 81.78 Billion in 2024, to achieve a value of USD 149.24 Billion by 2034.

The global in vitro diagnostics market is expected to grow at a CAGR of 6.20% during the forecast period 2025-2034, driven by increasing demand for advanced diagnostic facilities and a dramatic shift towards rapid testing.

Key drivers include the growing prevalence of chronic and infectious diseases, rising demand for early detection, and increased adoption of point-of-care and non-invasive diagnostic tools.

Rising use of personalized medicine, automation in laboratories, and increased adoption of IVD technologies in homecare and remote testing environments are key emerging trends.

Major regional market include North America, Europe, Asia Pacific, Latin America and the Middle East and Africa.

The main products include instruments, reagents and consumables, and software and services, each supporting laboratory testing and clinical diagnostics functions.

Applications include infectious diseases, oncology, diabetes, cardiology, nephrology, autoimmune diseases, drug testing, and various other clinical conditions.

End-users include clinical laboratories, hospitals, pharmaceutical and biotechnology companies, blood banks, and others.

The diverse applications for market are infectious diseases, diabetes, oncology, cardiology, drug testing/pharmacogenomics, HIV/AIDS, autoimmune diseases, and nephrology, among others.

The end users for the industry consist of hospital and clinics, diagnostic laboratories, point-of-care testing, and academic institutes, among others.

The major players in the industry are Danaher Corp, bioMérieux, Inc., Siemens Healthcare GmbH, ARKRAY America, Inc., Sysmex Corporation, and F. Hoffmann-La Roche Ltd, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2024 |

| Historical Period | 2018-2024 |

| Forecast Period | 2025-2034 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product |

|

| Breakup by Specimen |

|

| Breakup by Techniques |

|

| Breakup by Application |

|

| Breakup by Test Location |

|

| Breakup by End User |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 3,299

USD 2,969

tax inclusive*

Single User License

One User

USD 5,499

USD 4,949

tax inclusive*

Five User License

Five User

USD 6,999

USD 5,949

tax inclusive*

Corporate License

Unlimited Users

USD 8,199

USD 6,969

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Our step-by-step guide will help you select, purchase, and access your reports swiftly, ensuring you get the information that drives your decisions, right when you need it.

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.

Australia

63 Fiona Drive, Tamworth, NSW

+61-448-061-727

India

C130 Sector 2 Noida, Uttar Pradesh 201301

+91-723-689-1189

Philippines

40th Floor, PBCom Tower, 6795 Ayala Avenue Cor V.A Rufino St. Makati City,1226.

+63-287-899-028, +63-967-048-3306

United Kingdom

6 Gardner Place, Becketts Close, Feltham TW14 0BX, Greater London

+44-753-713-2163

United States

30 North Gould Street, Sheridan, WY 82801

+1-415-325-5166

Vietnam

193/26/4 St.no.6, Ward Binh Hung Hoa, Binh Tan District, Ho Chi Minh City

+84-865-399-124

United States (Head Office)

30 North Gould Street, Sheridan, WY 82801

+1-415-325-5166

Australia

63 Fiona Drive, Tamworth, NSW

+61-448-061-727

India

C130 Sector 2 Noida, Uttar Pradesh 201301

+91-723-689-1189

Philippines

40th Floor, PBCom Tower, 6795 Ayala Avenue Cor V.A Rufino St. Makati City, 1226.

+63-287-899-028, +63-967-048-3306

United Kingdom

6 Gardner Place, Becketts Close, Feltham TW14 0BX, Greater London

+44-753-713-2163

Vietnam

193/26/4 St.no.6, Ward Binh Hung Hoa, Binh Tan District, Ho Chi Minh City

+84-865-399-124

Share